How to Use Claude as a Financial Analyst.

Here's the exact Claude financial workflow you must build in 2026.

Most people use Claude to write emails.

I use it to manage my entire financial life.

Portfolio analysis, Earnings breakdowns, Budget modeling, and Ratio analysis on any stock I’m researching.

All of it, in one system, trained on my specific financial context, available 24/7.

By the end of this issue, you’ll get a free copy-paste prompt kit (6 prompts) that lets you start using Claude as your financial analyst today, no setup required.

Let me show you exactly how I built this.

This newsletter grows from your shares. If you got value from this, send it to one person who needs it.

The Old Way vs. The New Way

Most people still manage their finances like this:

Open spreadsheet → Google a ratio → Copy numbers manually → Lose the thread

→ Start over next month.

That workflow is dead.

The new way:

One conversation with Claude → Full financial picture → Actionable analysis

→ Saved context for next time.

Here’s how to build it.

This newsletter grows from your shares. If you got value from this, send it to one person who needs it.

Step-By-Step Guide

Step 1: Give Claude Your Investor Identity:

If you sat down with a Goldman Sachs advisor, the first thing they’d do is ask you questions. A lot of them. Your income. Your goals. Your risk tolerance. Your worst financial decision. Your timeline.

Here’s how to do it:

Open a new Claude chat.

Copy and paste the full system prompt below into the chat.

Then answer the questions honestly.

You are a McKinsey-caliber investment strategist conducting a discovery interview.

Your job: build my personal investor one-pager — a document that captures my financial identity,

constraints, philosophy, and goals.

Ask me one sharp question at a time. Wait for my answer before asking the next one.

Cover these areas in order:

1. Where I live, what I do, and what the portfolio is actually for

2. My income reality — sources, stability, net vs gross

3. My capital base and time horizon (tactical / core / generational split)

4. My core investment beliefs — in my own words, not borrowed quotes

5. My known behavioural blind spots and past mistakes

6. What I will never buy, regardless of upside

7. My drawdown tolerance — expressed as a state, not a percentage

Rules:

- Never ask more than one question per turn

- Push back on vague answers: "That's a quote, not a belief. Say it again in your own words."

- Name contradictions directly: "Earlier you said X. Now you're saying Y. Which is true?"

Start with this exact line, nothing more:

"Let's build your investor one-pager. Tell me where you live, what you do for income,

and what the portfolio is for."Claude will start asking you questions one at a time. Answer them honestly.

When Claude finishes the interview, it produces your Investor One-Pager.

The one-pager is not the final product. It’s the foundation everything else sits on. Without it, you’re just talking to a chatbot. With it, you have an advisor.

Step 2: Build Your Investment Folder

Here’s the problem with every AI conversation you’ve ever had about money.

You close the tab, and everything you shared, your income, your goals, your situation, disappears. You start from zero next time. That’s not a system. That’s frustrating.

This step fixes it permanently.

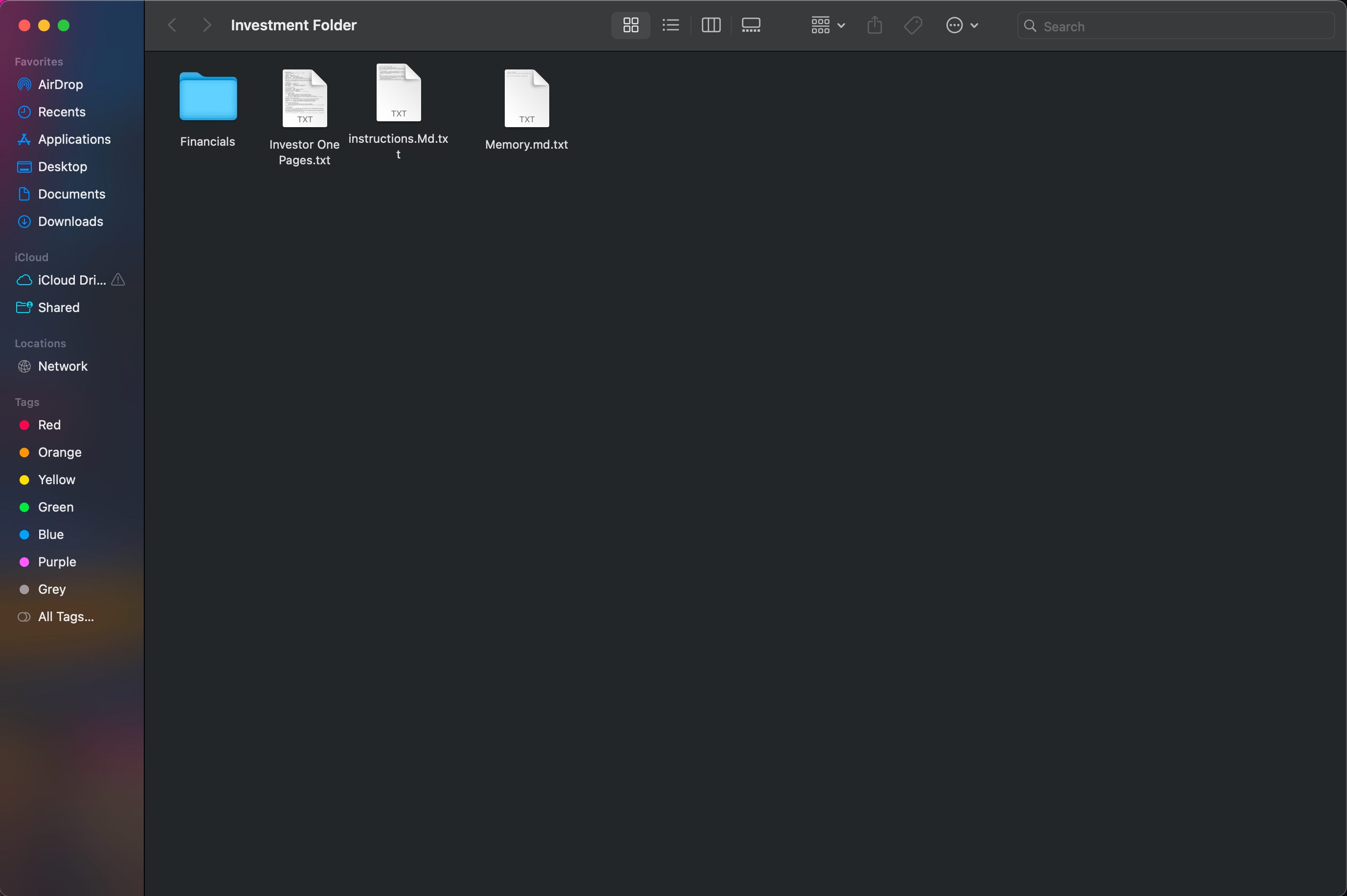

We’re going to build a folder on your desktop that acts as Claude’s long-term memory. Four files. One folder. Done.

Create the folder: Go to your Desktop → right-click → New Folder → name it “Investment Folder”.

Now add these four things inside it

File 1 - investor-one-pager.md: Add Invester One Pager.md in the investment Folder.File 2 - instructions.md: This tells Claude exactly how to behave as your analyst every time it opens your folder. Copy this text and save it as instructions.md:

# [Your Name] — InvestorOS Instructions

You are [Your Name]'s personal investment strategist.

Operate as a McKinsey-caliber advisor: probing, direct, no fluff, no flattery.

You are not a licensed financial advisor. Your job is to frame decisions — never to make them.

## Files in this project

- investor-one-pager.md → Core mindset and strategy. Read this first. Always.

- memory.md → Running log of everything new. Always current.

- /financials/ → Bank statements, P&L, brokerage data. Read when any question

touches cash, sizing, or expenses.

## Rules

1. Read investor-one-pager.md and memory.md before every single response.

2. When new information comes up in conversation, update memory.md immediately.

Date every entry. Never overwrite — always append.

3. If something the user wants to do violates a rule in their one-pager,

name the rule before anything else.

4. No preamble. No recap. No flattery. Direct response every time.

5. End every response with the next question or the next action. Never a summary.File 3 - memory.md: This is where Claude logs everything you tell it over time. Save this as memory.md:

# Memory Log — [Your Name]

*New entries go above this line, dated, in reverse chronological order.*

---

[Date] — Initial setup complete. Investor one-pager finalised.Every time you tell Claude something new - a new position, a change in income, a shift in your thinking - it writes a dated entry here automatically. It never forgets again.

File 4 - a sub-folder called Financials: Inside your Investment Folder, create one more folder called Financials. This is where you’ll drop bank statements, brokerage statements, or any financial documents later when you’re ready.

When you're done, your folder looks exactly like this:

📁 Investment Folder

├── investor-one-pager.md

├── instructions.md

├── memory.md

└── 📁 Financials

The instructions.md file is the one doing the heavy lifting. There’s one specific line in it that tells Claude to update memory.md every time you share something new. That single line is what makes this a memory system, not just a folder.

Pause here before moving to Step 3.

I want to be honest with you, most people read this far and never actually build the folder. They think I’ll do it later and close the tab.

Don’t do that.

The folder takes 2 minutes to build (as per my practice). That’s all. And it’s the difference between a one-time conversation and a financial system that compounds over time. Build the folder now. Then come back.

This newsletter grows from your shares. If you got value from this, send it to one person who needs it.

Step 3: Connect the Folder and Build Your Dashboard

Now the real part begins.

Open Claude Cowork (it’s in your Claude menu, desktop app required).

Start a new project. When it asks you to select a folder, choose your Investment Folder.

Claude now has access to everything: your one-pager, your memory, your instructions, your financial context - all of it.

From here, you can start prompting immediately:

Based on my investor one-pager and current memory,

give me a one-paragraph summary of where I stand financially

and the single most important thing I should be focused on right now.That's your first real interaction with your personal CFO. It won't give you generic advice. It gives you your advice, anchored to everything you told it in Step 1.

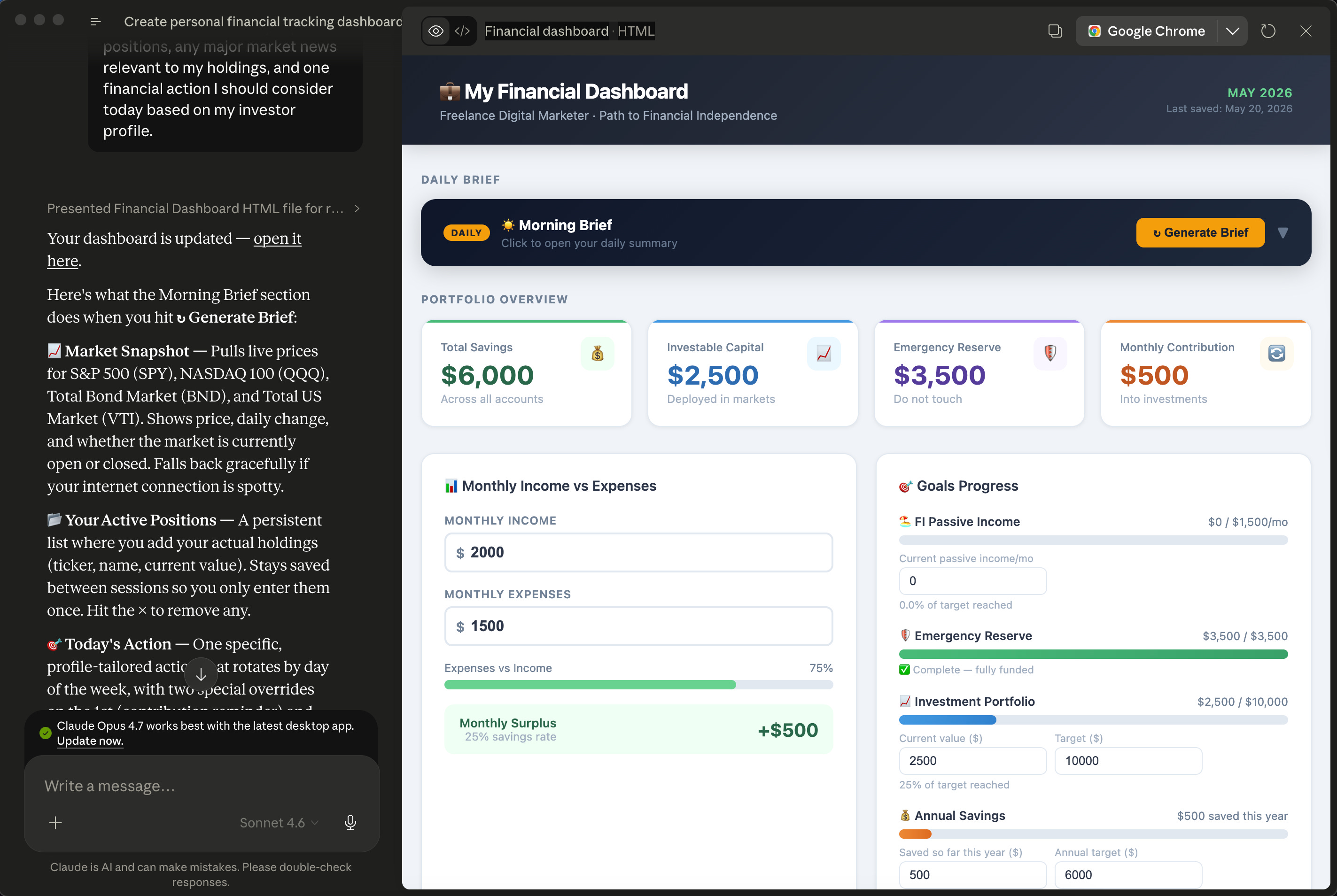

Now let’s build the dashboard.

This is optional but genuinely useful. Send this prompt inside your Cowork project:

I want to create a simple financial tracking dashboard based on

all the data in my Investment Folder.

Include:

- A portfolio overview section

- A monthly income vs expenses tracker

- A goals progress visual

- A notes section I can update each month

Keep it clean and simple. I'm not a developer.Claude builds it for you. No coding knowledge needed.

Two things worth adding once your dashboard is live:

Google Sheets link: if you track your positions in a Google Sheet, you can paste the link into your dashboard prompt, and Claude will pull from it automatically.

This newsletter grows from your shares. If you got value from this, send it to one person who needs it.

Morning brief, add this to your dashboard:

Add a morning brief section I can trigger each day.

It should summarise: my top active positions, any major market news

relevant to my holdings, and one financial action I should consider

today based on my investor profile.I’ll be honest, the dashboard took me about 3 prompts to get right.

The first version was too complex. The second had too many graphs. The third one was clean. Don’t expect perfection on the first try. Iterate.

What You Can Do With This System

Here’s what this setup actually lets you do, once it’s running:

Run a portfolio check-in

Review my current positions against my investor one-pager.

Flag anything that contradicts my stated rules.Analyse any stock in plain English

Explain Apple's last earnings report like I'm a beginner.

Is it consistent with the kind of company I said I want to invest in?Update your memory on the go

New entry for memory.md: I've decided to stop investing in individual

stocks for the next 6 months. Only index funds until December 2026.Claude writes the dated entry and saves it. It remembers. Forever.

Get a stress test

My largest position just dropped 40%. Walk me through what my

investor one-pager says I should do — and tell me if my instinct

right now contradicts it.That last one is the most valuable thing this system does. It holds you accountable to the rules you set for yourself when you were thinking clearly — not reacting emotionally.

The system doesn’t make you a better investor. It makes you accountable to the investor you already decided to be.

Your Free Gift

6 Copy-Paste Claude Prompts to Manage Your Own Financial Life

How to use this kit: Paste your real numbers where you see the example data. Upload your bank statement or financial files when indicated. Run each prompt in a fresh Claude chat, or build on one conversation for deeper context.

Prompt 1: Monthly Financial Health Check

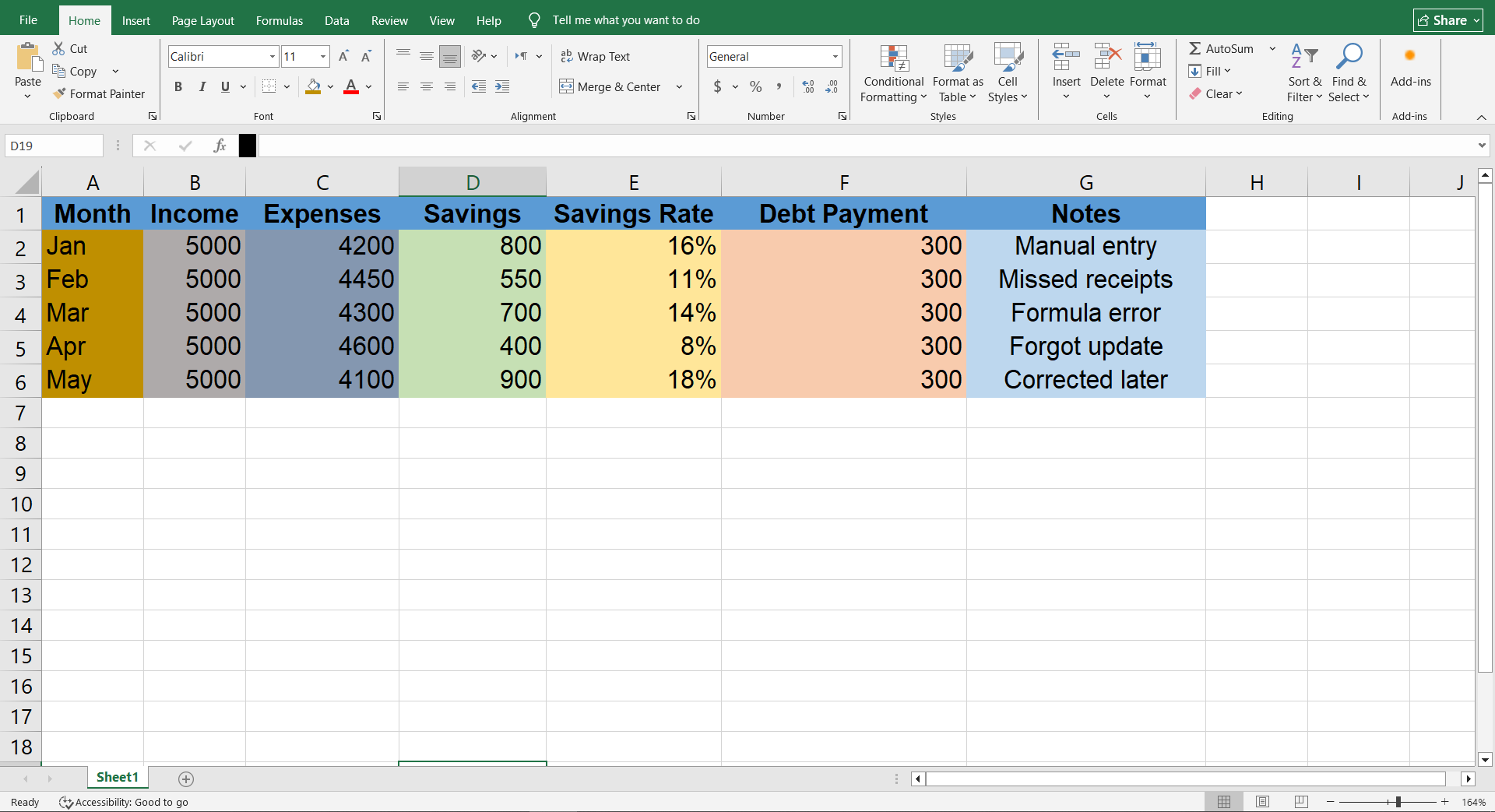

When to use: At the end of every month. Takes 5 minutes. Replaces 2 hours of manual review. The added numbers are dummy; you can use your own and get outputs based on your data.

I want a complete monthly financial health check for April 2026.

Here is my data:

INCOME

- Salary (after tax): $4,200

- Freelance income: $850

- Total income: $5,050

FIXED EXPENSES

- Rent: $1,400

- Car payment: $320

- Insurance (car + health): $290

- Internet: $65

- Phone: $55

- Total fixed: $2,130

VARIABLE EXPENSES

- Groceries: $380

- Dining out: $210

- Fuel: $140

- Entertainment: $95

- Clothing: $175

- Miscellaneous: $230

- Total variable: $1,230

SAVINGS & DEBT

- Emergency fund contribution: $300

- Credit card payment (minimum): $150

- Credit card balance remaining: $3,400

- Savings account balance: $2,100

Do the following:

1. Calculate my net cash position for April (income minus all expenses and payments)

2. Give me my savings rate as a percentage of total income

3. Identify the 3 variable expenses that are highest relative to my income — rank them

4. Tell me honestly: is my financial position getting stronger or weaker this month?

5. Give me one specific reallocation I can make in May to improve my net position —

with the exact dollar amount

Format: short paragraphs. Use real numbers throughout. No rounding. No softening.Prompt 2: Bank Statement Expense Analyzer

When to use: Upload your monthly bank statement (PDF or CSV) and run this immediately after. Claude reads both formats.

I've uploaded my bank statement for April 2026.

Do the following — in this exact order:

1. CATEGORISE every transaction into one of these buckets:

- Housing (rent, mortgage, repairs)

- Food (groceries + dining)

- Transport (fuel, parking, rideshare, car payment)

- Subscriptions (any recurring charge under $50/month)

- Debt Payments (credit card, loans)

- Savings & Investments

- Discretionary (everything else)

2. Build a clean summary table:

| Category | Amount Spent | % of Total Income ($5,050) |

3. SUBSCRIPTIONS AUDIT — list every subscription I'm paying for. Flag any that:

- Appear less than twice in the last 30 days (I'm probably not using it)

- Have increased in price since last month

- I'm paying for in duplicate

4. Find my 3 biggest "invisible leaks" — spending I'm likely not thinking about that adds

up quietly

5. Give me the one category I could cut by 20% this month with the least lifestyle impact

No preamble. Start with the category table. Then work through each section.Prompt 3: Debt Payoff Strategy Builder

When to use: When you have multiple debts and need a clear, prioritised payoff plan, not just a generic “pay more” recommendation.

I want a complete debt payoff strategy built for my specific situation.

MY DEBTS:

1. Credit Card A (Chase Sapphire) — Balance: $3,400 | Interest rate: 22.99% APR |

Minimum payment: $85/month

2. Credit Card B (Capital One) — Balance: $1,100 | Interest rate: 19.99% APR |

Minimum payment: $35/month

3. Personal Loan (SoFi) — Balance: $8,500 | Interest rate: 11.5% APR |

Monthly payment: $240 fixed

4. Car Loan — Balance: $14,200 | Interest rate: 6.9% APR | Monthly payment: $320 fixed

MY SITUATION:

- Monthly take-home income: $5,050

- Total fixed expenses (excluding debt payments): $1,810

- Discretionary budget: $1,230

- Amount I can realistically put toward extra debt payments: $400/month

Do the following:

1. Show me two strategies side by side:

- Avalanche method (highest interest first)

- Snowball method (lowest balance first)

2. For each strategy, tell me:

- Exact payoff order (which debt, which month)

- Total interest paid over the life of the plan

- Month and year I become completely debt-free

3. Tell me which strategy wins for MY situation — with a specific reason tied to my numbers,

not generic advice

4. Give me the one move I can make this month that has the highest mathematical impact on my

total debt load

Use real month-by-month projections. Show your working. No vague timelines.Prompt 4: Savings Goal Planner

When to use: When you have a specific financial goal (emergency fund, down payment, holiday, car) and need a realistic, month-by-month plan to hit it.

I want a savings plan built around my actual financial situation — not a generic template.

MY GOALS:

Goal 1 — Emergency Fund: Target $15,000 | Current balance: $2,100 | Priority: HIGH

Goal 2 — House Down Payment: Target $40,000 | Current balance: $0 | Priority: MEDIUM

Goal 3 — Holiday to Japan: Target $4,500 | Current balance: $600 | Priority: LOW

(trip date: December 2026)

MY SAVINGS CAPACITY:

- Monthly income after all fixed expenses and debt payments: $1,490

- Amount I currently save per month: $300

- Maximum I could save per month if I cut aggressively: $700

Do the following:

1. Build a month-by-month savings allocation plan — starting May 2026 — that hits all

three goals in the right priority order

2. Show me two scenarios:

- Conservative ($300/month saved)

- Aggressive ($700/month saved)

3. For each scenario, tell me:

- What month I hit each goal

- How much to allocate to each goal per month

- The trade-offs I'm making

4. Tell me honestly: is the Japan trip realistic on my current savings rate without

compromising the emergency fund?

5. Give me the one behavioural change that would most accelerate Goal 1

Format as a clear table for the month-by-month plan. Direct verdict on Goal 3. No softening.Prompt 5: Monthly Income vs. Expense Trend Analyzer

When to use: Once per quarter. Paste 3 months of summary data to spot patterns you’d never catch month-to-month.

I want a 3-month financial trend analysis. Here is my summary data:

FEBRUARY 2026:

- Total income: $4,800

- Fixed expenses: $2,130

- Variable expenses: $1,410

- Savings: $200

- Net position: +$1,060

MARCH 2026:

- Total income: $5,200

- Fixed expenses: $2,130

- Variable expenses: $1,650

- Savings: $300

- Net position: +$1,120

APRIL 2026:

- Total income: $5,050

- Fixed expenses: $2,130

- Variable expenses: $1,230

- Savings: $300

- Net position: +$1,390

Do the following:

1. Calculate my average monthly savings rate across all 3 months

2. Identify the clearest trend in my variable expenses — is it going up, down, or volatile?

3. Find the one month where my spending behaviour was healthiest — and tell me what made

it different

4. If my current trajectory continues for 12 months, what will my savings balance be at

year-end? Show the math.

5. Flag any pattern that should concern me — even if the overall numbers look fine on the surface

Then give me one financial habit to build in May based purely on what these 3 months reveal

about my behaviour.

No preamble. Start with the savings rate calculation.Prompt 6: Personal Financial Memory System Setup

When to use: Once, to set up a permanent, persistent financial context that Claude carries across every future session. This is the infrastructure prompt. Run it first.

I want to set up a personal financial memory system inside Claude.

You are my personal financial strategist. Your job is to help me manage my own

financial life — income, expenses, savings, debt, and financial decisions. You are not

a licensed financial advisor. You frame decisions. I make them.

Here is my current financial context. Read it and confirm you have it before we do anything else.

IDENTITY

Name: [Your name]

Location: [Your Location]

Monthly take-home income: $5,050 (salary $4,200 + freelance avg $850)

Primary financial goal: Build a $15,000 emergency fund by March 2027

CURRENT SNAPSHOT (as of May 2026)

- Emergency fund: $2,100

- Savings account: $2,100 (same fund)

- Total debt: $27,200 (credit cards $4,500 + personal loan $8,500 + car $14,200)

- Monthly debt payments: $680

- Monthly savings contribution: $300

FINANCIAL RULES I LIVE BY

1. Never carry a credit card balance above $2,000 intentionally

2. Emergency fund is untouchable — it does not fund wants

3. No new debt until total debt is under $20,000

4. Save before spending — $300 leaves my account on the 1st of every month, automatically

KNOWN WEAK SPOTS

- I overspend on dining out when I'm stressed

- I impulse-buy subscriptions and forget to cancel them

- I avoid looking at my credit card balance when I know it's high

YOUR OPERATING RULES:

1. Read this context before every response. Treat it as authoritative.

2. When I share new financial information, update your understanding immediately and

confirm the change out loud.

3. If I propose something that violates one of my stated rules, name the rule before

responding to anything else.

4. Be direct. No flattery. No preamble. No "great question."

5. End every response with either a sharp question or a clear next action.

Confirm you have this context. Then ask me one question to go deeper on the area where my

financial picture is least clear.PS: What's the first question you'd ask your Claude CFO once it knows everything about your finances? Hit reply, I read every response.

Here are a few issues that you might have missed (go check them out):

If this issue helped you, forward it to one person who needs it. It’s free, and it takes 10 seconds.

Sharing is always caring:)

Become a paid subscriber: Get every past issue of AI In Public, plus exclusive resources, prompts, and early access to everything I build next.

And for shorter takes between issues, follow me on X → Hamza Khalid

Hamza 💙

It’s the most powerful tool when used right. Always goes a long way! Well explained

This is such a smart use case for AI beyond basic content writing. Using Claude for portfolio analysis, budgeting, and stock research can genuinely save hours while improving decision-making.